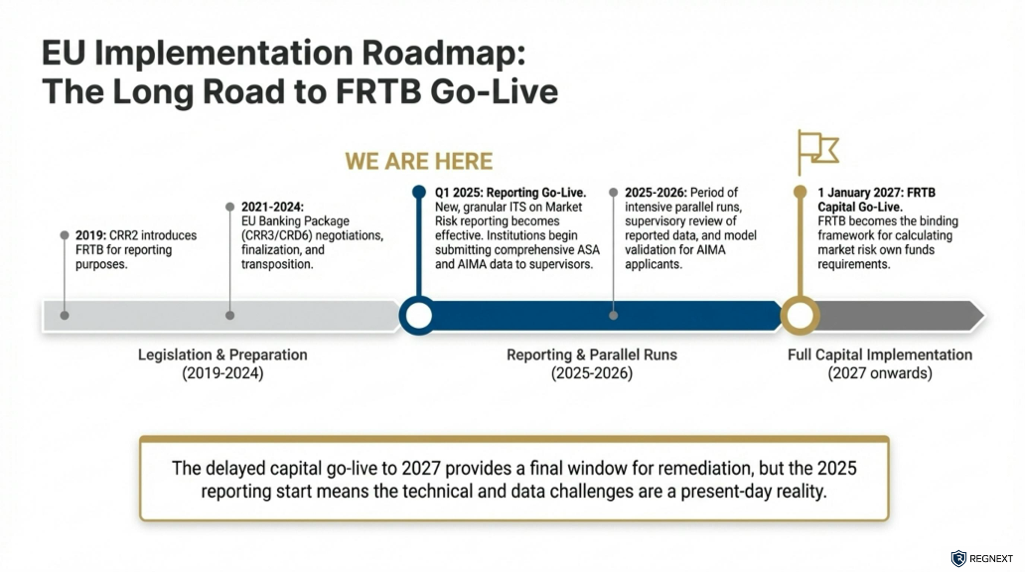

The implementation of the Fundamental Review of the Trading Book (FRTB) within the European Union represents the finalization of the Basel III reforms, aiming to address structural weaknesses in the calculation of capital requirements for market risk. While the legislative framework is established via the Capital Requirements Regulation (CRR III), the timeline for binding capital charges has undergone significant adjustments to protect the competitiveness of EU banks.

The European Commission has adopted a Delegated Regulation that postpones the date of application of the FRTB standards for the calculation of own funds requirements for market risk until 1 January 2027.

This decision extends previous delays (which initially targeted 2026) and is driven by the mandate to ensure an international level playing field. Trading and market-making activities are highly globalized, and the Commission monitors implementation progress in other major jurisdictions to prevent competitive distortions. Specifically, the United States has faced delays in finalizing its implementation of the Basel III standards, prompting the EU to align its timeline to avoid disadvantaging European institutions.

Despite the delay in binding capital charges, the regulatory machinery remains active. The "Banking Package" entered into force on 9 July 2024, and the postponement specifically targets the capital calculation aspect of FRTB.

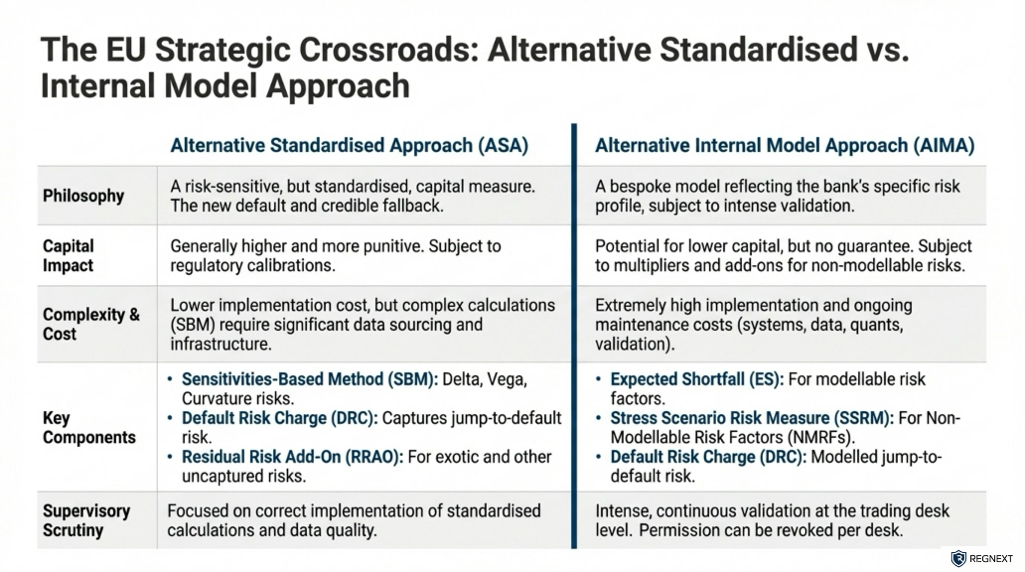

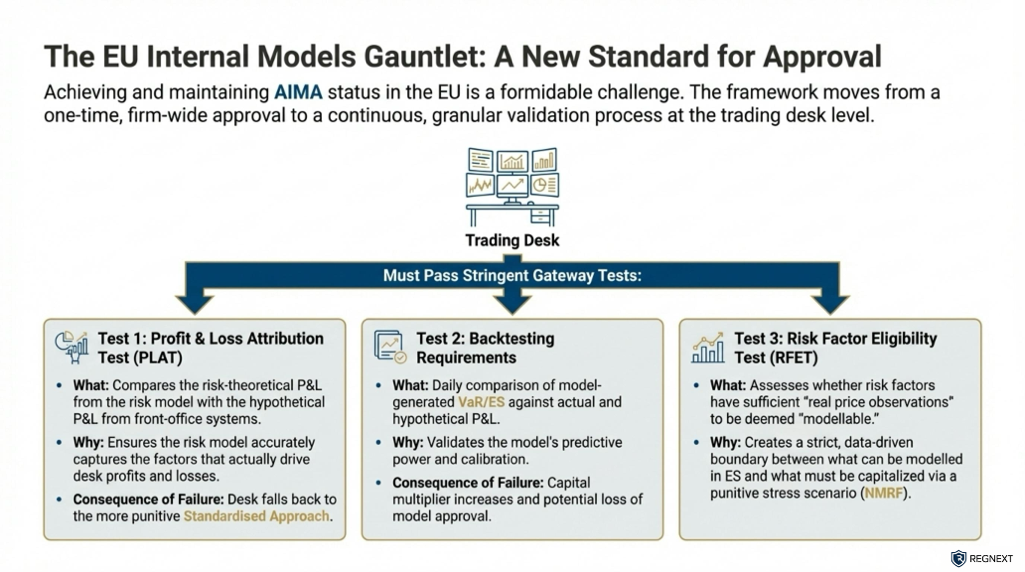

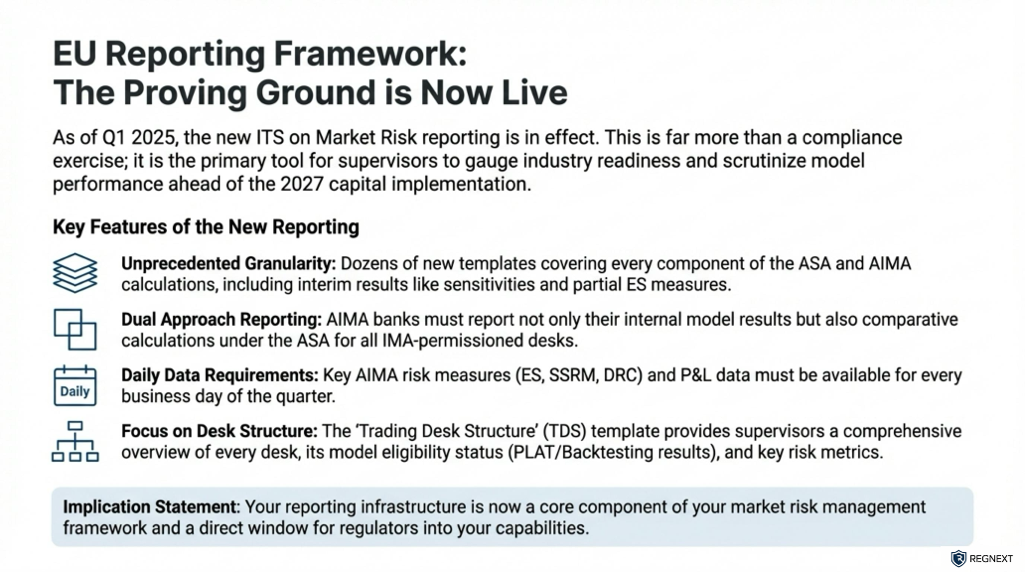

1. Continued Reporting RequirementsThe delay decouples the legal application of capital requirements from operational readiness. Banks cannot pause their implementation projects. During the postponement period, institutions must continue to report calculation results to competent authorities based on the FRTB framework. This effectively serves as a mandatory "dry run," allowing supervisors to monitor readiness and validate the new calculation engines (Alternative Standardised Approach and Alternative Internal Model Approach) before they impact capital ratios.

2. The Output FloorThe implementation of the Basel III "Output Floor"—a floor for capital requirements calculated using internal models—proceeds. However, because the FRTB capital charge is delayed, the Commission expects EU banks using internal models to calculate the market risk component of the output floor by comparing their current internal models against the FRTB Standardised Approach.

3. Trading Book BoundaryNew requirements regarding the boundary between the trading book and the non-trading (banking) book were set to apply from 1 January 2025. However, because the capital calculations based on these boundaries are delayed, the Commission has indicated that supervisors should take action to avoid a staggered implementation that would require banks to apply new boundary rules to pre-FRTB capital calculations, which could lead to unintended consequences.

The shift to January 2027 signals that while the EU remains committed to the Basel III standards, it will not proceed unilaterally in a way that harms its banking sector’s global standing. For compliance teams, this "delay" is not a pause; it is an extended testing period. The mandatory reporting requirements ensure that when the switch is finally flipped in 2027, banks must be fully operational with the more sophisticated risk measurement techniques inherent in the FRTB.