Based on the new sources provided, here is the reviewed and updated executive summary.

Key Updates Incorporated:

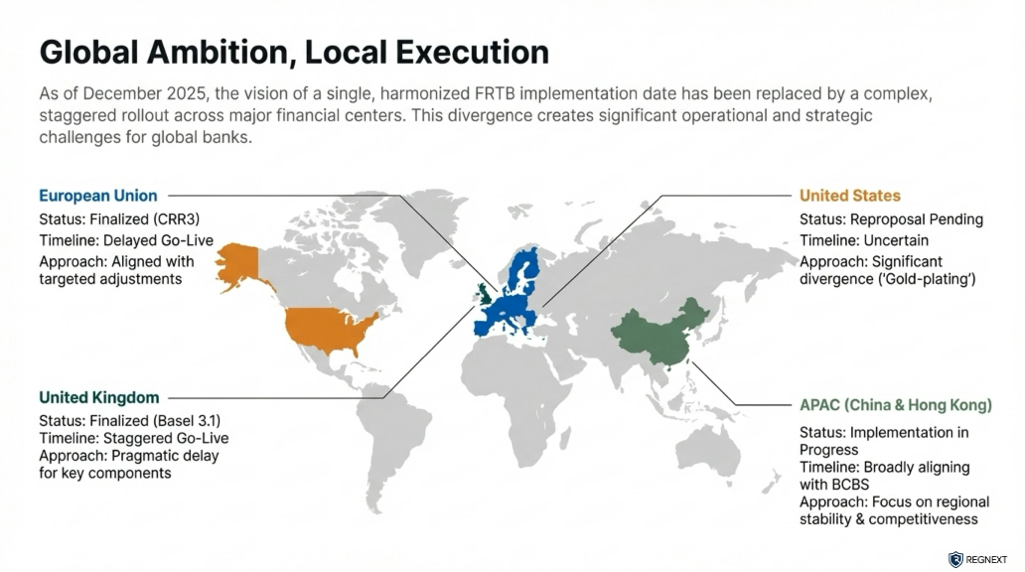

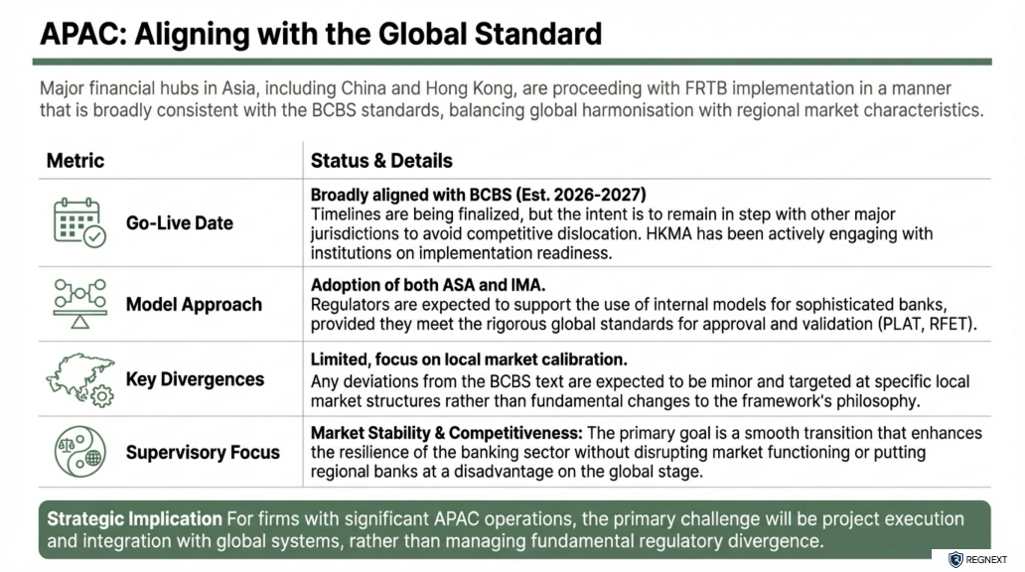

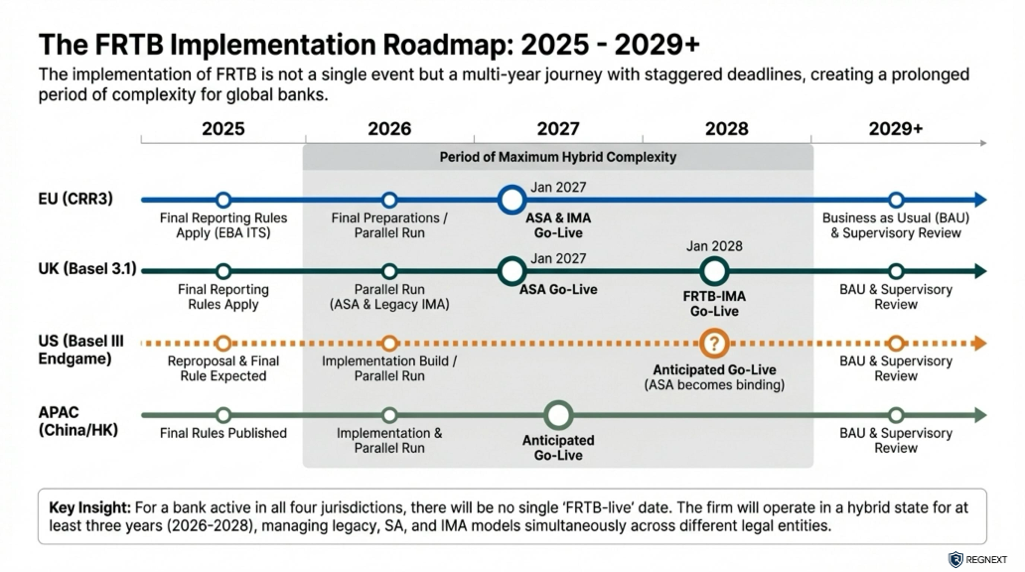

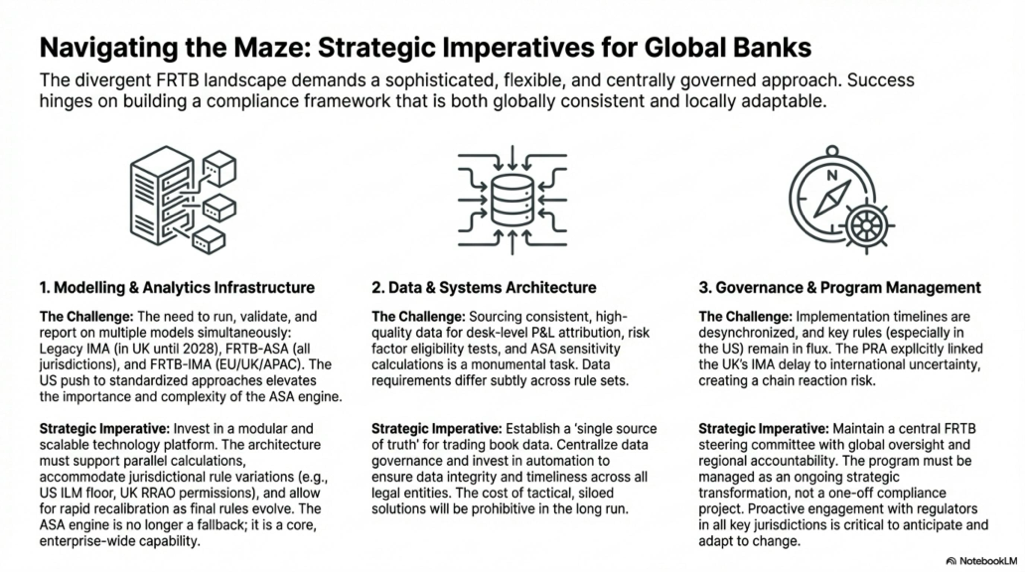

The implementation of the Fundamental Review of the Trading Book (FRTB) has shifted from a coordinated global rollout to a fragmented timeline. While Hong Kong has proceeded with a 1 January 2025 implementation, Western jurisdictions have significantly delayed enforcement to protect domestic banking competitiveness.

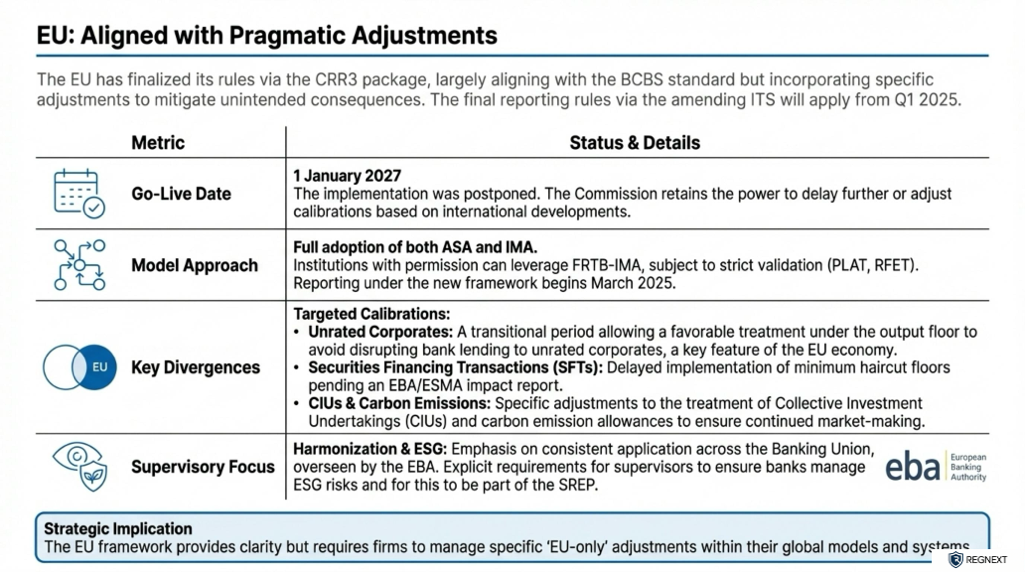

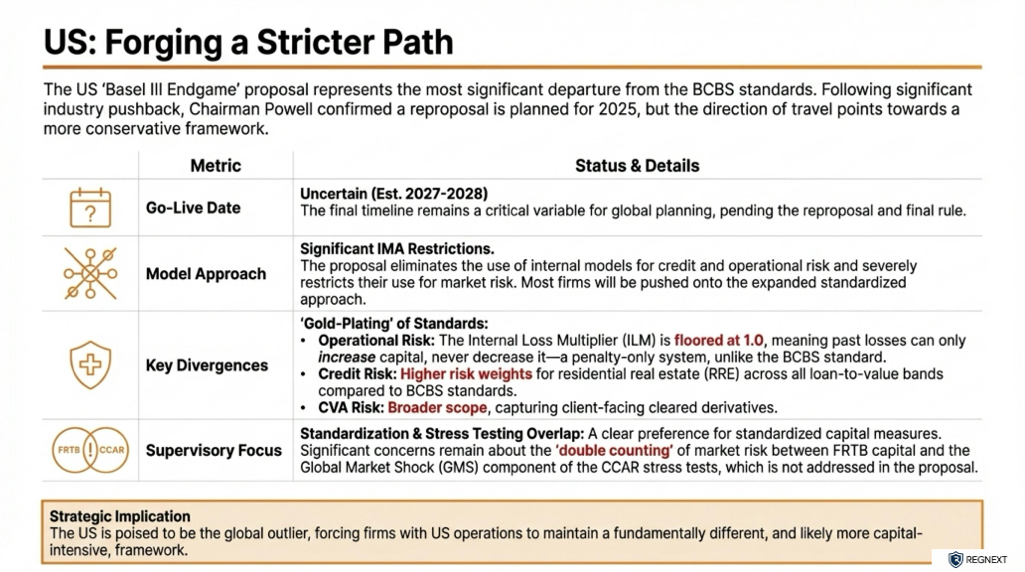

In a major development, the European Commission adopted a Delegated Regulation on 12 June 2025, postponing the application of the market risk capital requirements by one year to 1 January 2027. This decision explicitly cites the need to preserve a "international level playing field" given the uncertainty surrounding U.S. implementation. Meanwhile, the United States has signaled a restart of its rulemaking process; Federal Reserve Chair Jerome Powell indicated in early 2025 that the "Basel III Endgame" will be re-proposed, leaving the U.S. compliance date indefinite.

1. The U.S. "Gold-Plating" and ReproposalThe U.S. divergence has deepened. The original 2023 proposal was criticized for "gold-plating" (exceeding) international standards, such as prohibiting internal models for credit risk and imposing higher risk weights on residential mortgages (up to 20 percentage points higher than Basel III),. With the confirmed reproposal of these rules, the U.S. is currently the furthest behind in the implementation cycle.

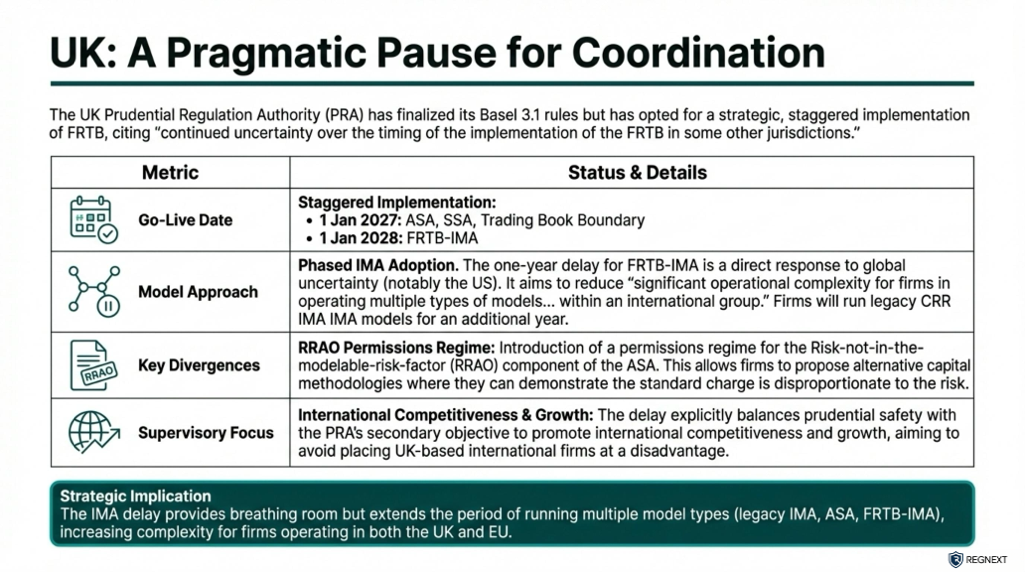

2. Strategic Delays in Europe (EU & UK)Both the EU and UK have effectively decoupled their timelines from the original Basel schedule to wait for the U.S. The EU's delay to 2027 is a direct response to the U.S. delays, ensuring EU banks are not subject to higher capital requirements for trading activities before their American competitors.

3. Operational Risk & Internal Loss Multiplier (ILM)A major technical divergence involves the Internal Loss Multiplier (ILM) for operational risk. The EU has exercised discretion to set the ILM to 1, effectively neutralising the impact of historical operational losses on capital requirements. The U.S. proposal, conversely, set a minimum ILM of 1, meaning U.S. banks with historical losses would face strictly higher capital charges.

4. Treatment of Structural FXThe EU is finalizing specific technical standards (RTS) for "Structural FX" positions to allow banks to exclude certain foreign exchange positions from capital requirements if they are taken to hedge capital ratios. This specific relief is being heavily standardized in the EU to ensure a level playing field, whereas other jurisdictions may treat these hedges differently under national discretions.