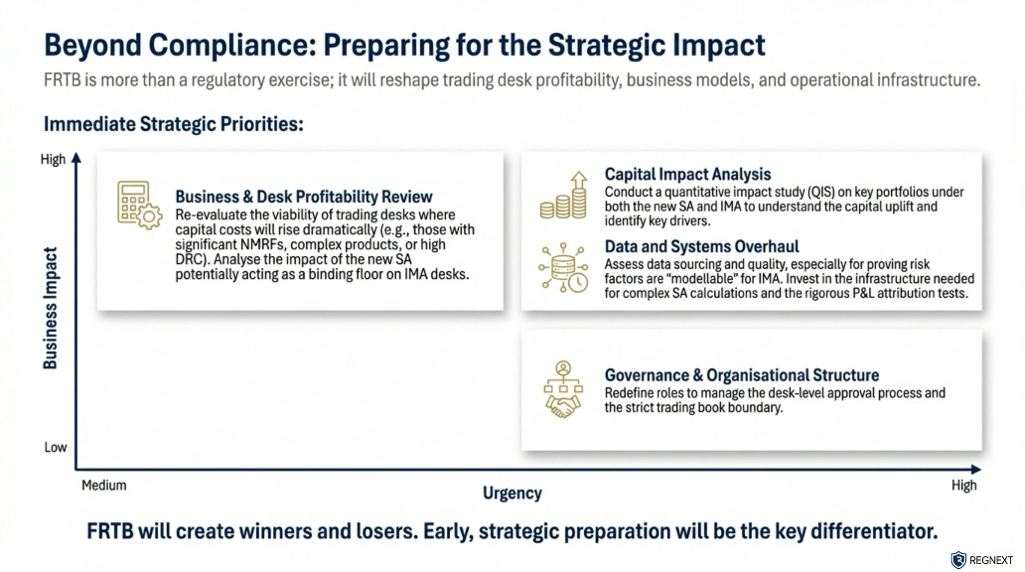

Executive Summary: The UK’s Implementation of FRTB

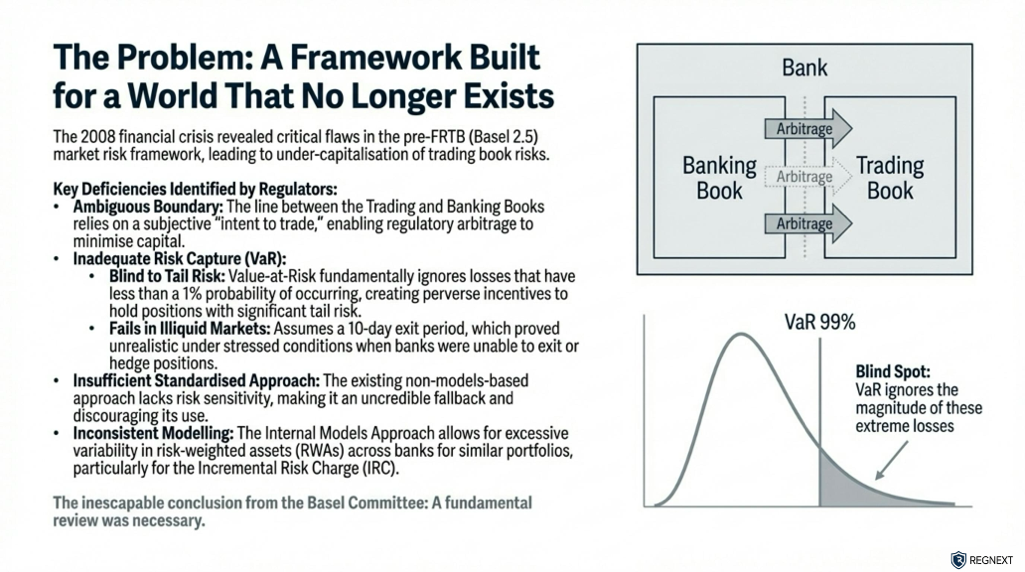

The Fundamental Review of the Trading Book (FRTB) represents a comprehensive overhaul of the capital requirements for market risk. As part of the wider Basel 3.1 package, the UK Prudential Regulation Authority (PRA) is implementing these standards to address structural flaws exposed by the 2007–09 financial crisis, specifically the under-capitalization of trading book exposures.

The UK’s approach is characterized by a segmented implementation timeline, prioritizing a robust standardized capital floor before transitioning to complex internal models.

1. The Split Implementation Timeline

To balance international competitiveness with financial stability, the PRA has established a phased timeline for FRTB adoption:

- Phase 1: January 1, 2027 (Standardised Approach & Output Floor): The main elements of Basel 3.1, including the new rules for the Trading Book Boundary and the revised Standardised Approaches (SA), will enter into force. Crucially, the 72.5% Output Floor becomes active on this date. This requires all firms, including those using internal models, to calculate and report risk-weighted assets (RWAs) using the Standardised Approach to determine the binding capital floor.

- Phase 2: January 1, 2028 (Internal Models Approach): The implementation of the FRTB Internal Models Approach (FRTB-IMA) has been proposed to be delayed by one year. In the interim (2027), firms will calculate Pillar 1 capital requirements using their existing (legacy) market risk models, while simultaneously reporting under the new Standardised Approach for the Output Floor.

2. Key Methodological Pillars

The UK framework introduces three primary changes to market risk calculation:

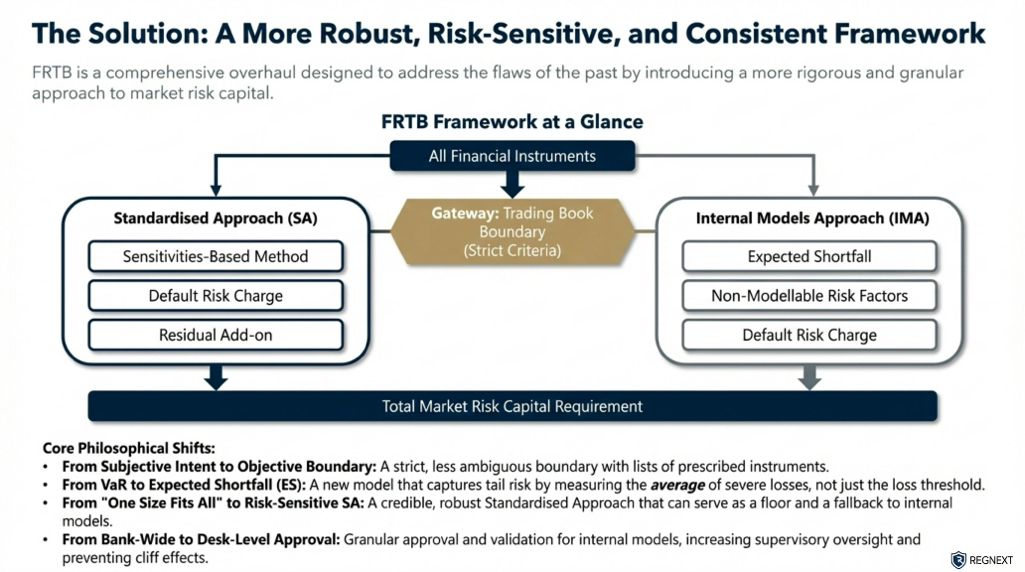

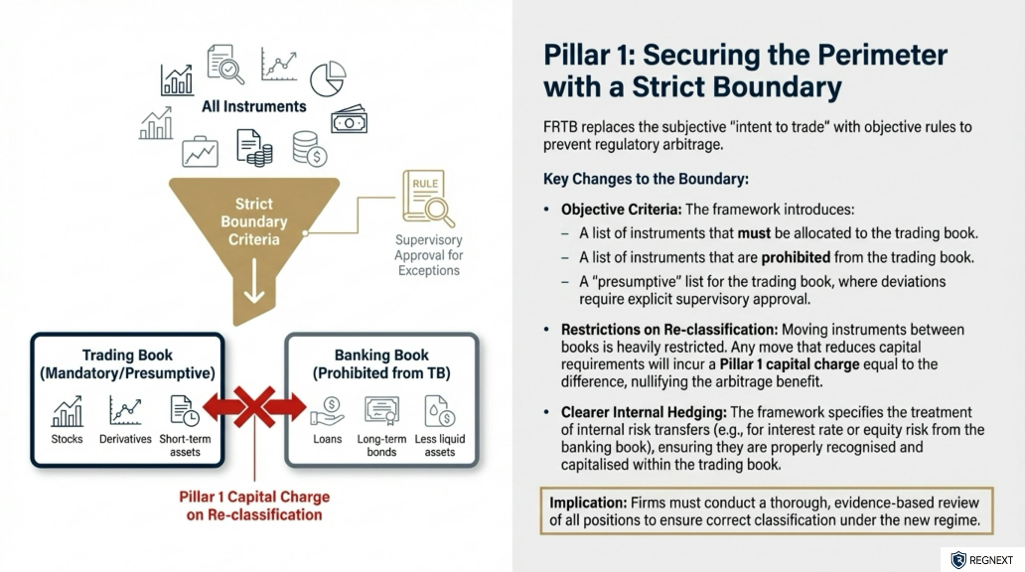

- The Trading Book Boundary: The new regime implements stricter criteria for assigning instruments to either the trading or banking book to prevent regulatory arbitrage. Operational simplifications have been proposed for Collective Investment Undertakings (CIUs) to reduce cliff-edge effects when classifying funds.

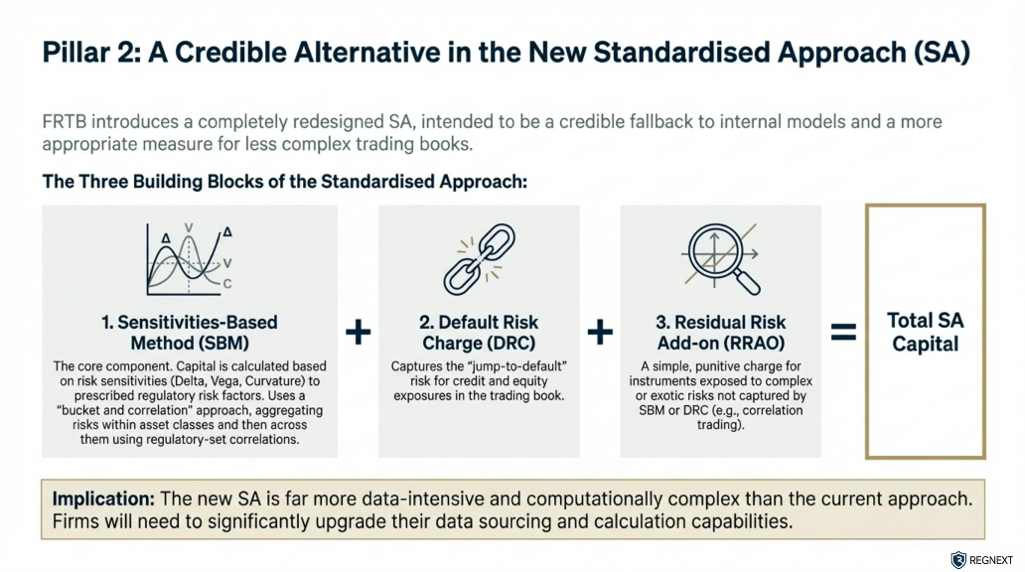

- The Standardised Approach (SA): The SA has been recalibrated to be more risk-sensitive. It serves as a credible fallback to internal models and calculates the Output Floor. Firms with limited derivatives business may use a Simplified Standardised Approach (SSA), while others must use the Advanced Standardised Approach (ASA). A new permissions regime has been proposed for the Residual Risk Add-On (RRAO) within the ASA to prevent disproportionate capital charges for exotic risks.

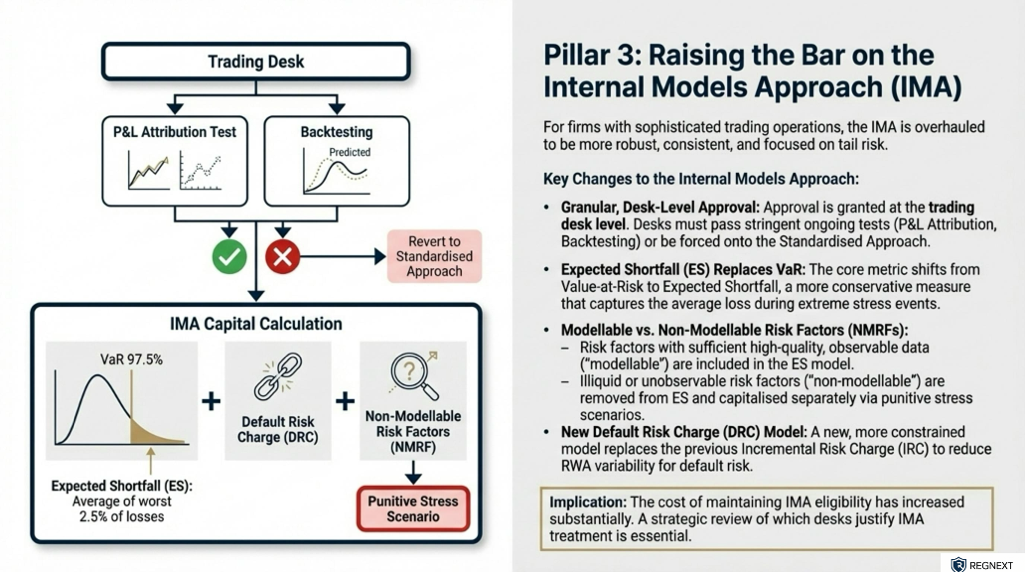

- The Internal Models Approach (IMA): The FRTB-IMA replaces Value-at-Risk (VaR) with Expected Shortfall (ES) to better capture tail risk and market illiquidity. Crucially, model approval is now required at the trading desk level, allowing supervisors to withdraw approval for specific desks without invalidating the entire model. Existing IMA permissions will generally not be saved; firms must apply for new permissions under the FRTB-IMA rules.

3. FCA Investment Firms

For investment firms regulated by the Financial Conduct Authority (FCA) rather than the PRA, market risk is governed by the Investment Firms Prudential Regime (IFPR). This regime utilizes the K-factor approach, specifically K-NPR (Net Position Risk), which is derived from the UK CRR market risk rules. While distinct from the banking regime, the FCA’s methodology for market risk remains dependent on the wider UK adoption of FRTB standards.

Conclusion

The UK’s strategy effectively elevates the Standardised Approach to a binding constraint from January 2027. Firms must prepare for parallel compliance: operating legacy models for capital setting in 2027 while finalizing the data-intensive FRTB-IMA infrastructure for the 2028 deadline.