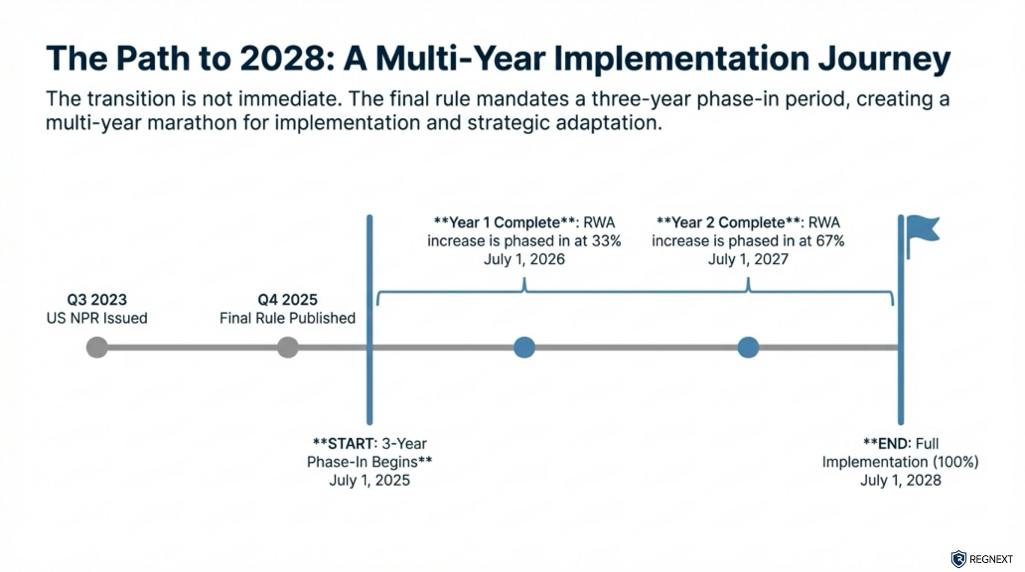

OverviewThe United States is currently in the process of implementing the Fundamental Review of the Trading Book (FRTB) as part of the broader "Basel III Endgame." On July 27, 2023, the Federal Reserve (FRB), the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC) issued a joint Notice of Proposed Rulemaking (NPR) to revise capital requirements for large banking organizations.

The proposal applies primarily to banking organizations with total assets of $100 billion or more and those with significant trading activity (defined as $5 billion in trading assets/liabilities or exceeding 10% of total assets). The stated goal is to standardize capital requirements, reduce regulatory arbitrage, and better capture tail risks exposed during the Global Financial Crisis.

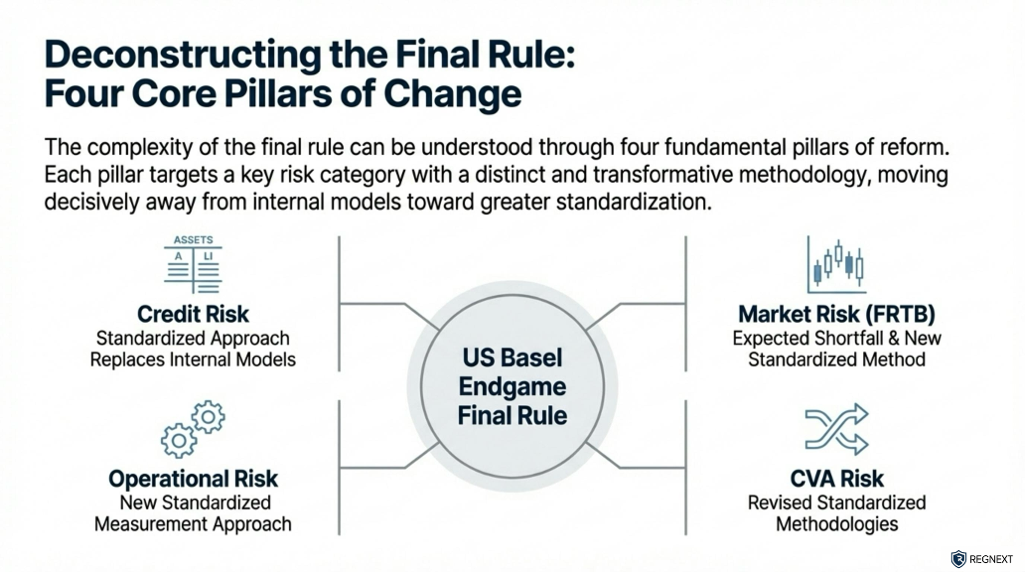

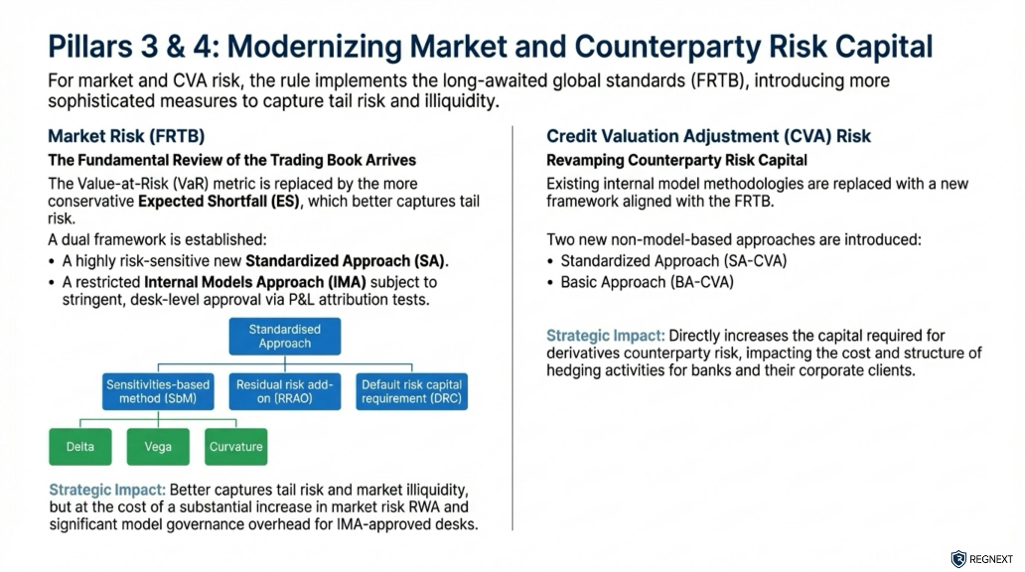

Key Technical ShiftsThe US proposal replaces the current market risk framework with a "revised approach" that aligns with the core mechanics of the international Basel standards:

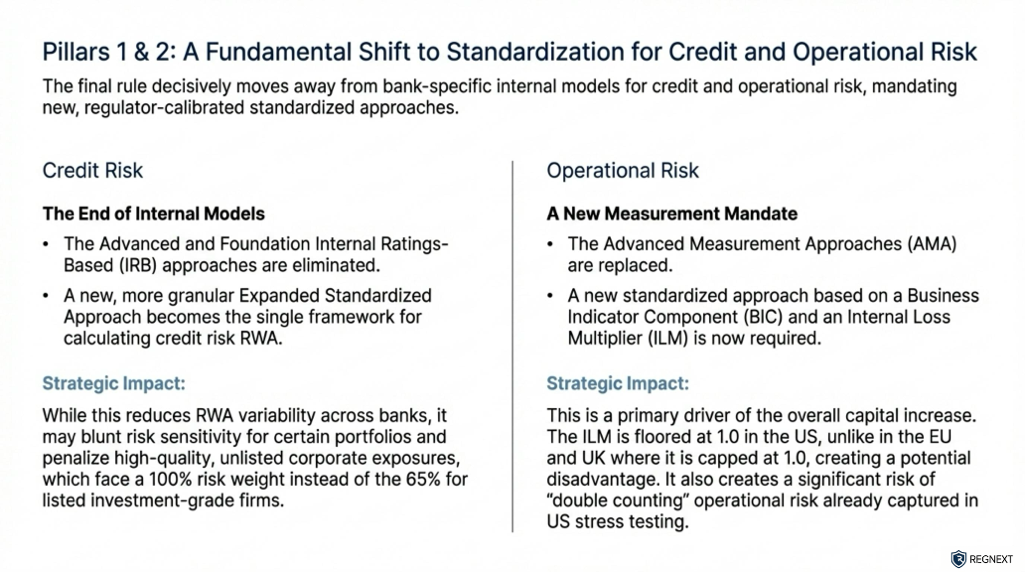

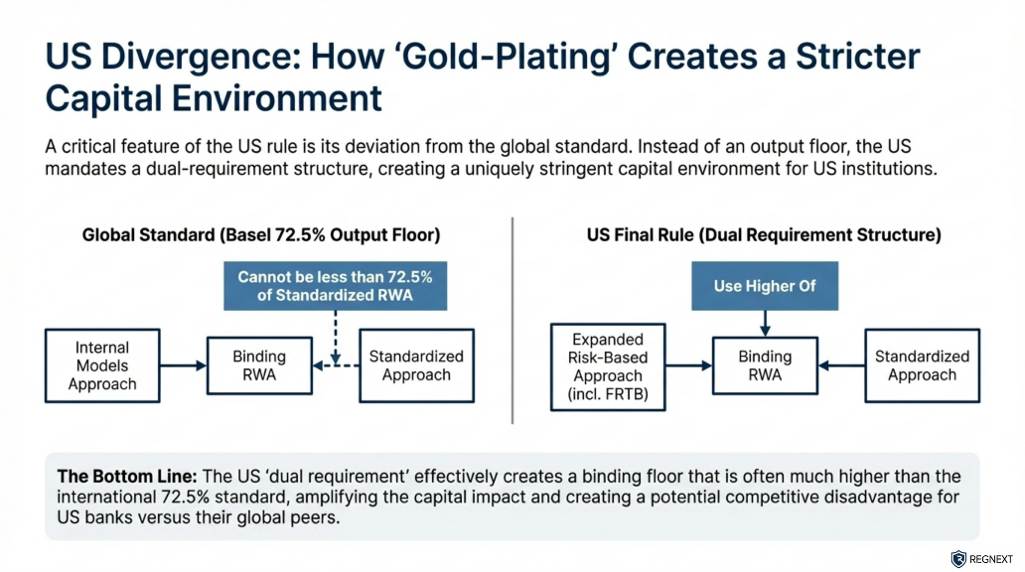

US-Specific Deviations ("Gold-Plating")The US implementation introduces stricter requirements than the international Basel agreement, often referred to as "gold-plating". Key deviations include:

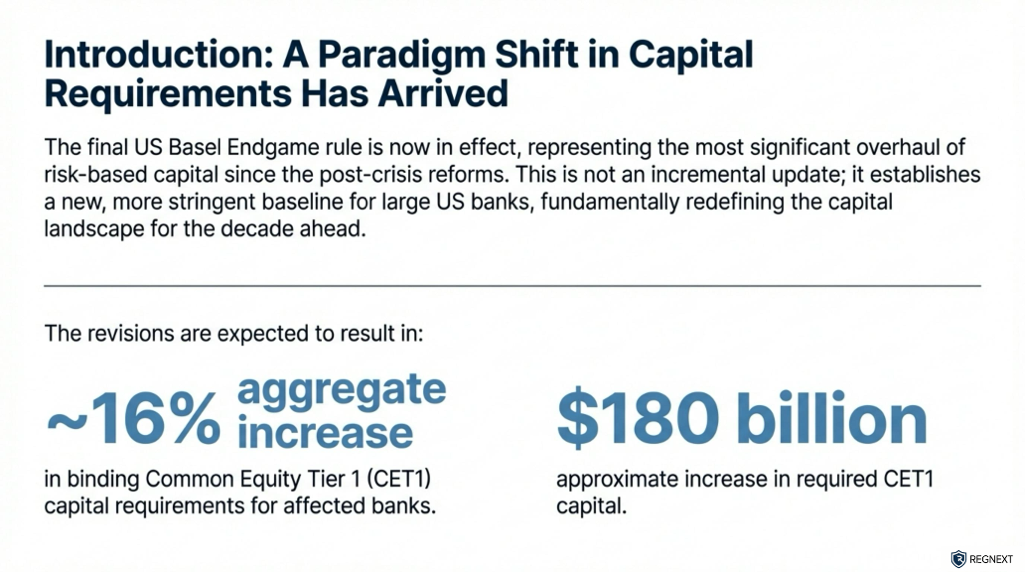

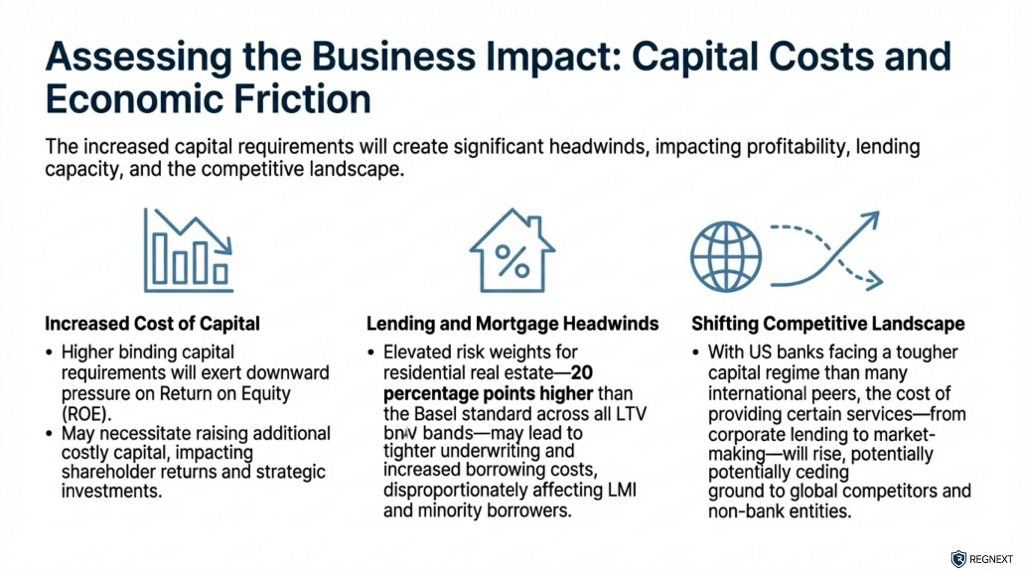

Economic Impact and ControversyRegulators estimate the proposal will increase Common Equity Tier 1 (CET1) capital requirements by approximately 16% for large holding companies, with G-SIBs facing increases up to 19%. Industry analysis suggests the increase for trading activities specifically could be nearly 60% to 80%.

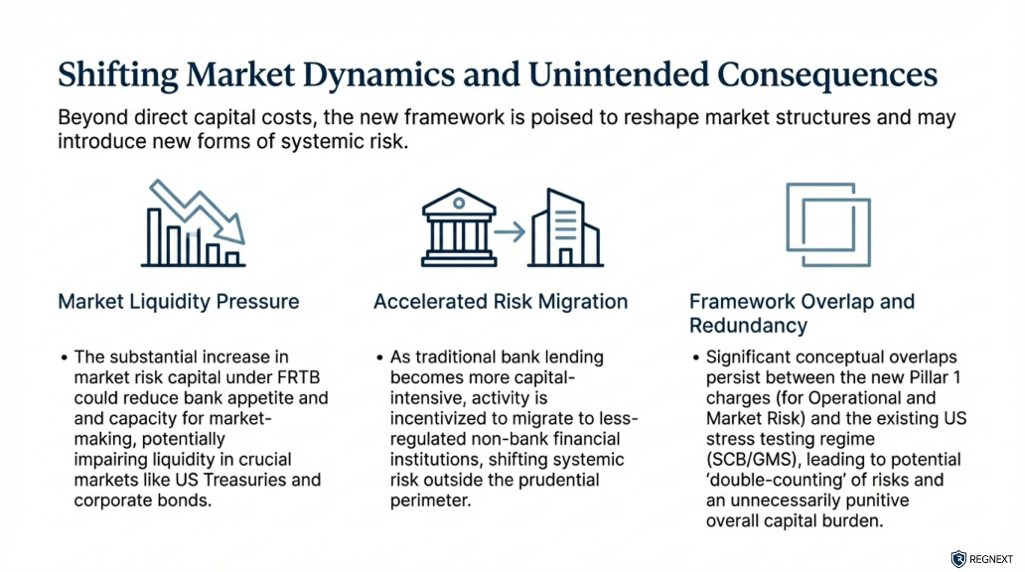

Critics argue that the FRTB overlaps with the Global Market Shock (GMS) component of US supervisory stress tests, effectively double-counting market risk. Furthermore, there are concerns that increased capital costs will reduce market liquidity, increase hedging costs for end-users (such as farmers and pension funds), and accelerate the migration of activity to the non-bank financial sector.

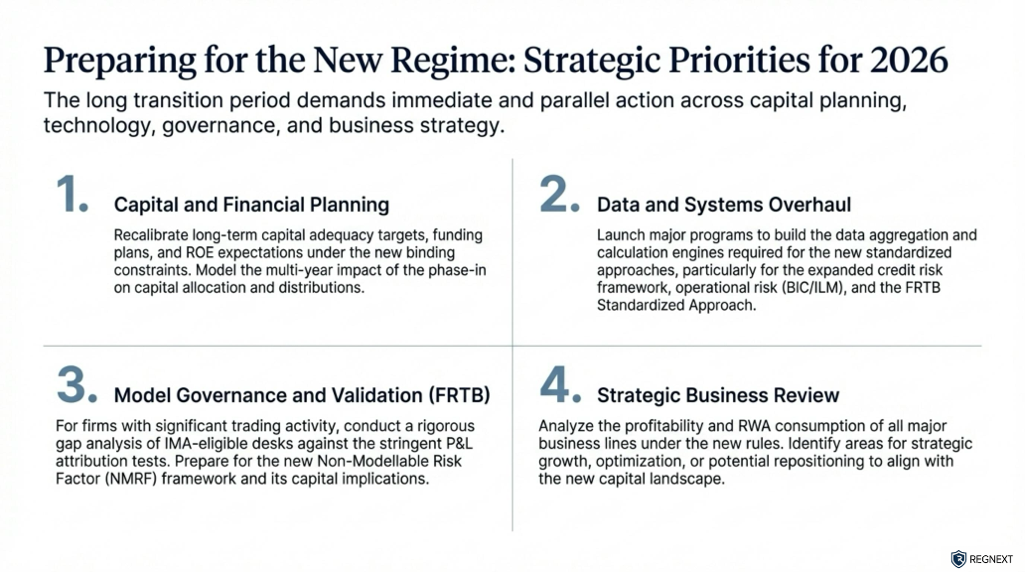

TimelineThe proposed transition period is scheduled to begin on July 1, 2025, with full compliance required by July 1, 2028.