Executive Summary: FRTB Implementation in Hong Kong and Mainland China

Strategic Context: Definitive Adoption vs. Global DelaysIn sharp contrast to the regulatory uncertainty in the United States and the delayed timelines in the European Union, Hong Kong and Mainland China have proceeded with definitive, accelerated implementation schedules for the Fundamental Review of the Trading Book (FRTB). Both the Hong Kong Monetary Authority (HKMA) and the National Financial Regulatory Administration (NFRA) have finalised their statutory frameworks, positioning the Greater China region as an early adopter of the Basel III market risk standards.

Hong Kong: Full Basel Alignment with Rigorous GovernanceThe HKMA has established a definitive "go-live" date of January 1, 2025, for the revised market risk capital framework. The regulatory architecture is codified in the Supervisory Policy Manual (SPM) modules MR-1 (Market Risk Capital Charge) and MR-2 (CVA Risk Capital Charge), issued in March 2024.

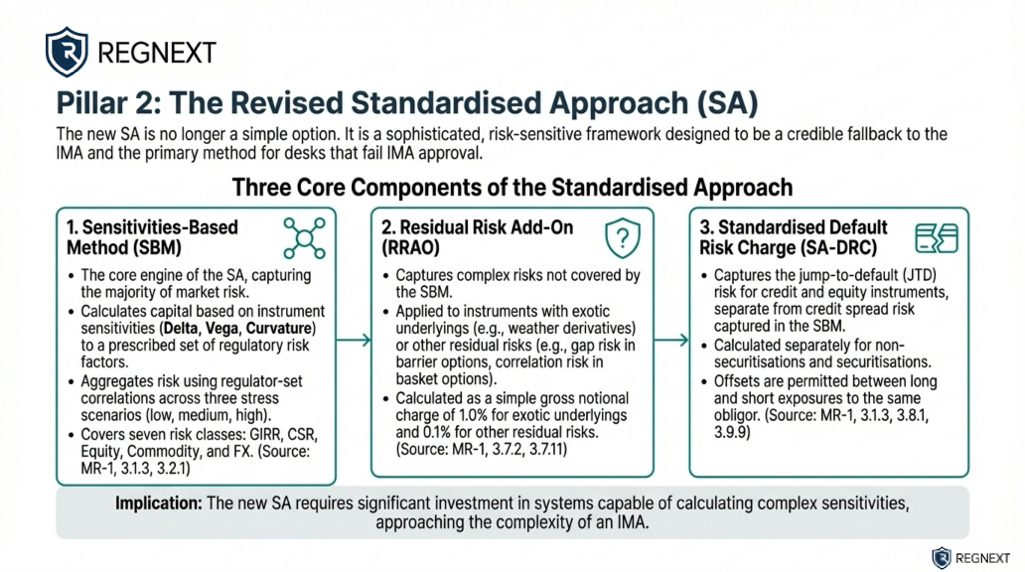

- Methodological Optionality: The HKMA framework provides Authorized Institutions (AIs) with the full spectrum of Basel approaches. This includes the sophisticated Internal Models Approach (IMA) for advanced banks, the Standardised Approach (SA) as a credible fallback, and a Simplified Standardised Approach (SSA) for institutions with smaller, less complex portfolios.

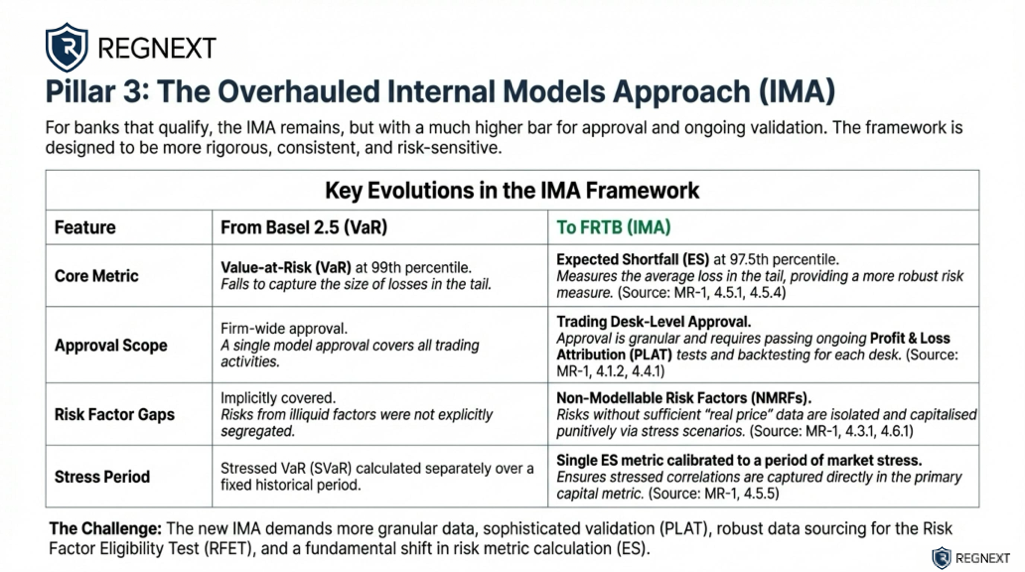

- Operational Demands: For banks aiming to utilise the IMA, the HKMA enforces rigorous continuous governance. Approval relies not just on initial validation but on passing ongoing Profit and Loss Attribution (PLAT) tests and backtesting requirements to ensure internal models accurately reflect the risks of individual trading desks.

- Reporting: To ensure readiness for the 2025 deadline, the HKMA mandated that AIs commence reporting under the new framework on a quarterly basis starting July 1, 2024.

Mainland China: A Conservative, "Correlation-Maximized" ApproachThe NFRA has adopted the Basel standards with a distinct, conservative local overlay intended to bolster systemic resilience. The primary regulatory text, the "Rules on Market Risk Management of Commercial Banks," was issued with an effective date of June 20, 2025.

- The "Correlation" Divergence: The most critical deviation in the Chinese framework appears in the technical rules for the Standardised Approach (Annex 14). While the Basel standard allows for a single calculation, the NFRA mandates that banks calculate the capital charge under the Sensitivities-Based Method (SBM) using three distinct correlation scenarios: High, Medium, and Low.

- Conservative Capitalisation: Crucially, banks must hold capital equivalent to the maximum charge resulting from these three scenarios. This requirement structurally embeds a stress buffer into the capital calculation, ensuring reserves are sufficient to withstand spikes in asset correlation during market turmoil.

- Implementation Focus: The Chinese framework places a heavy, immediate prescriptive focus on the Standardised Approach (SA), establishing it as the primary mandated threshold for commercial banks while the IMA framework matures.

Regional Implications for ComplianceFinancial institutions operating across the Greater China region must navigate a "one standard, two systems" reality. Compliance strategies must account for the HKMA’s emphasis on sophisticated model governance (PLAT/Backtesting) alongside the NFRA’s requirement for multi-scenario correlation stress testing, which will likely result in higher capital charges for Mainland trading books compared to standard Basel calibrations.