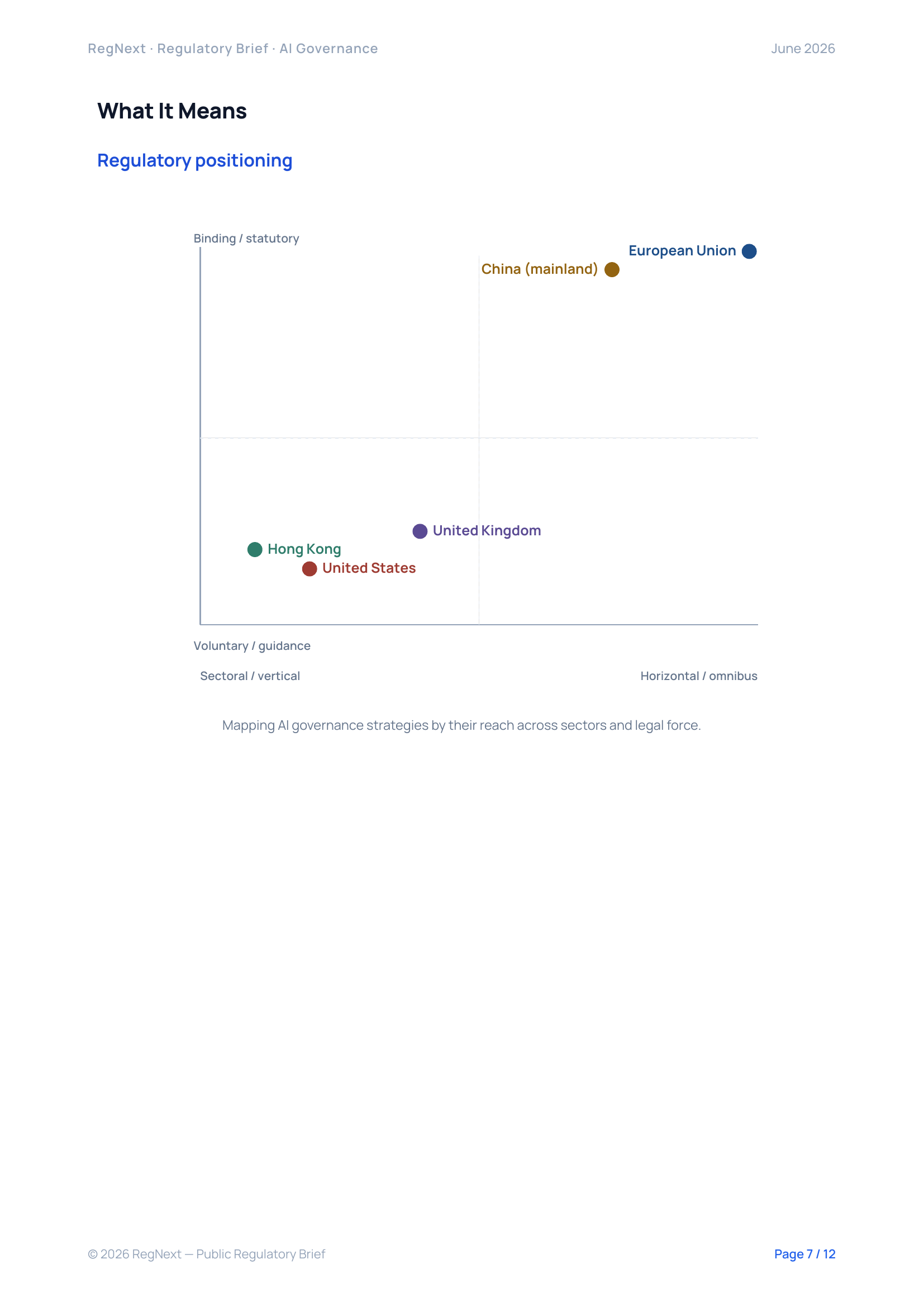

As at June 2026, the global artificial intelligence regulatory environment is becoming increasingly fragmented. The European Union continues to set the benchmark with a binding, risk-based AI Act, while the United States has moved toward a pro-innovation and deregulatory policy posture focused on AI leadership and competitiveness. The United Kingdom continues to rely on a sector-led model, while Mainland China and Hong Kong follow more service-specific and supervisory approaches.

For regulated firms, the challenge is no longer limited to interpreting individual AI rules. The operational challenge is maintaining a living inventory of AI use cases, obligations, controls, owners, evidence and jurisdictional change.

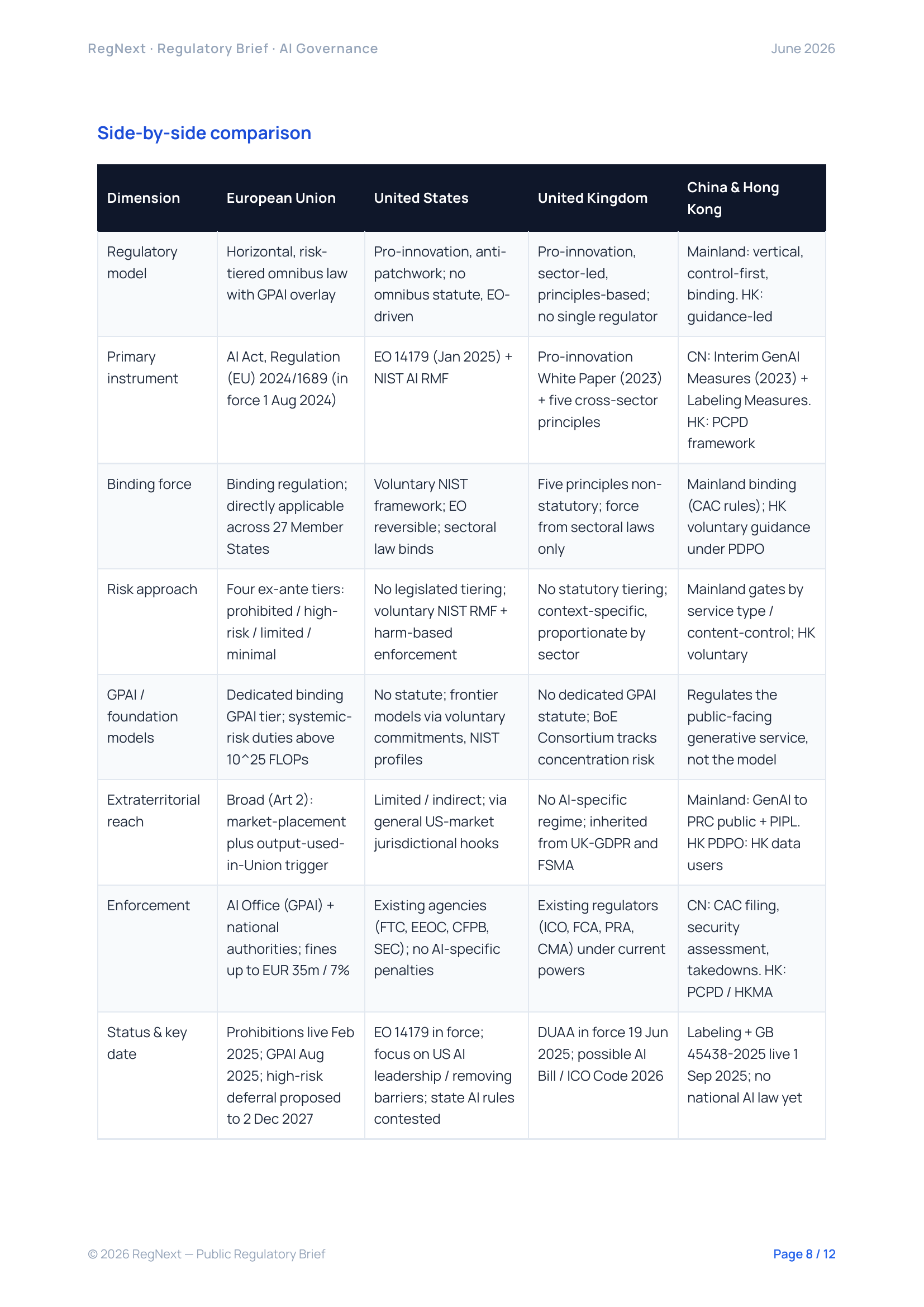

The European Union governs AI through Regulation (EU) 2024/1689, known as the AI Act. The framework is based on four risk tiers: prohibited, high-risk, limited-risk and minimal-risk AI systems. Prohibited practices became applicable in February 2025, while general-purpose AI obligations became applicable in August 2025. The EU Digital Omnibus package remains pending final adoption and publication, meaning firms should continue to treat the original AI Act application schedule as the planning baseline.

In the United States, federal AI policy has shifted toward AI leadership, innovation and the removal of regulatory barriers. Executive Order 14179 supports this pro-innovation posture, while EO 14365 seeks to address state-level regulatory fragmentation. In the absence of a comprehensive federal AI statute, existing agencies continue to apply sectoral laws to AI-related conduct, while NIST’s AI Risk Management Framework remains an important voluntary standard.

The United Kingdom continues to apply a pro-innovation, sector-led model. Rather than creating a single AI regulator, the UK relies on existing regulators to apply five cross-sector principles: safety, security and robustness; transparency and explainability; fairness; accountability and governance; and contestability and redress. For financial services, the FCA and Bank of England are integrating AI oversight into their existing supervisory mandates.

Mainland China follows a binding, control-first approach focused on generative AI services, algorithm recommendation, deep synthesis and AI-content labelling. Hong Kong follows a distinct, guidance-led approach focused on data privacy, financial-sector resilience, consumer protection and human-in-the-loop oversight.

Across jurisdictions, the direction of travel is clear: AI governance is becoming a regulatory execution problem. Firms need to move beyond static policy documents and build structured, auditable governance infrastructure covering AI use-case inventories, jurisdictional applicability, obligation mapping, control ownership, evidence management, incident monitoring and regulatory change.

The firms best positioned for the next phase will be those able to translate fragmented AI rules into controlled workflows, clear ownership, traceable evidence and auditable decision-making.

RegNext helps regulated firms bring structure, traceability and consistency to regulatory monitoring and compliance operations, converting fragmented regulatory developments into organised, decision-useful intelligence.